Fairbourne Capital · October 2019

WeWork Was the Exception, Not the New Rule

In a twist of fate, it was an 86-year-old US law that ultimately destroyed the value of one of the quickest start-ups in history to reach nearly a $100 billion dollar valuation — WeWork. The law was the requirement in the US for firms looking to IPO to file an S-1, or prospectus, which reveals details of the financial results and operations of a firm. The statement by Softbank this week that it was throwing WeWork a lifeline post the recent failed IPO was a victory for the public market investors as the underlying fundamentals of WeWork didn't match a $100 billion dollar company.

However, this is not the end of the staying private for longer until a jumbo IPO trend with WeWork following in the footsteps of Uber, Slack, Pinterest, etc.

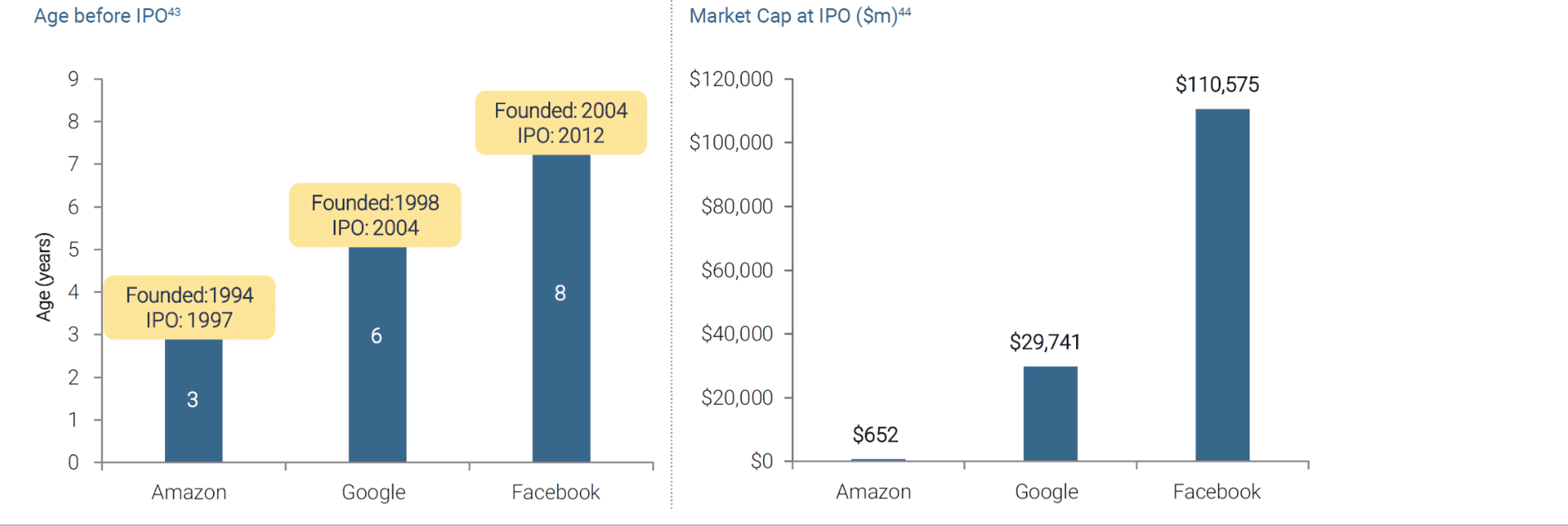

Long gone are the days when firms would follow Amazon IPO'ing at a <$1 billion valuation in order to obtain the capital to grow, providing savers and pension funds with the outsized returns of successful real innovators. There will be a company staying private long enough to achieve a $100 billion equity valuation at IPO before the end of this cycle. Amazon has ultimately delivered returns of 2,250x since the 1997 IPO, but if they would have waited as Facebook and others did, the returns investors would have achieved would have been closer to 10x. Still a good return, but it's a long way from 2,250x and is an indication that a small group of private market investors are creaming the best returns.

In one way WeWork was following the strategy of Amazon that if one industry player attracts the most capital and its valuation gets large enough, this low cost of capital can ensure that there won't be enough oxygen left in the room for anyone else to survive much less grow. The “de-oxygenation” strategy is now tried and tested to great effect when regulators are asleep at the wheel and is driving valuations far more than EBITDA or profits for several industries, and not just tech. The decline in anti-trust enforcement and rise in industry concentration is quite broad based in the US. Think of not just WeWork or Amazon, but Uber, Apple, Anheuser-Busch, airlines, Google, Facebook… their valuations have helped them grow fast and acquire potential competitors and it's a reason so few companies have managed to be so important in our daily lives.

The de-regulation of private markets has completely broken the trade-off between going public to get access to large pools of capital and staying private. The historically lower cost of capital achieved by public companies in exchange for meeting regulatory and disclosure requirements has been flipped on its head by the migration of capital towards private markets. Public companies now run the risk of facing a higher cost of capital than their private counterparts.

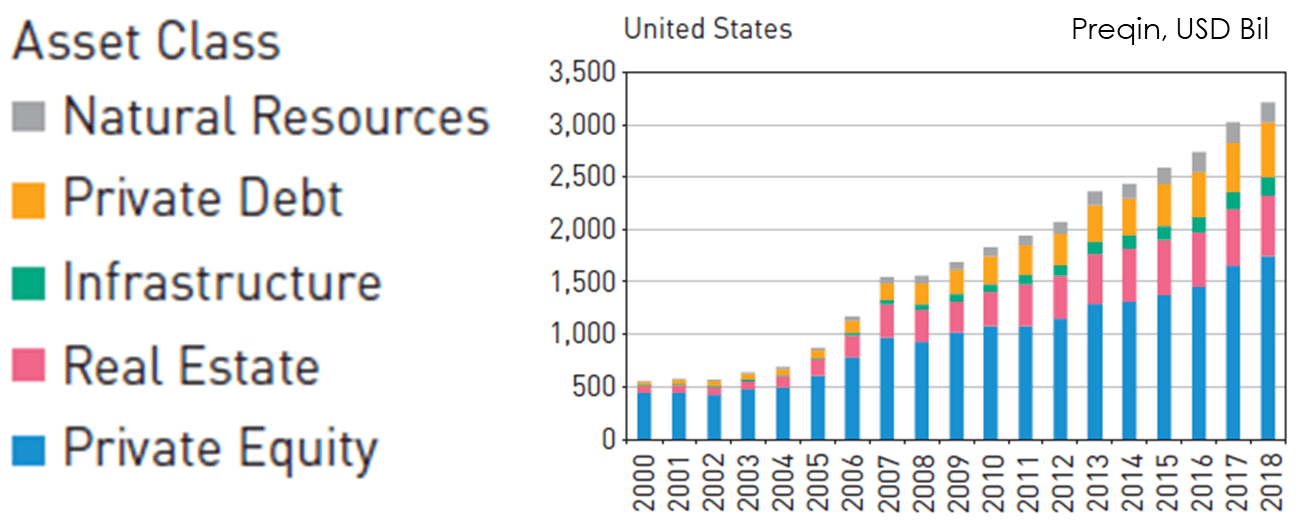

Beyond de-regulation, low cost passive funds and ETFs has resulted in the creation of a “risk free” equity asset class where capital allocations are referenced to recognised benchmarks by trustees doing their fiduciary duty. Significant pools of capital are now investing parts of their equity risk allocations into privates, private equity funds, VC funds, private debt, infrastructure, thematic ETF tilts, etc. instead of actively managed public equity funds. Institutional investors have alternatives and they are using them in droves.

What is remaining in the public markets is largely a risk free equity allocation which needs to be liquid, very liquid, to perform its function as an equity exposure parking place until more interesting opportunities appear, consigning many mid-cap and small-cap firms to a much smaller pool of potential investors with valuations well below their intrinsic value.

While the PE and other alternative funds get paid well to invest capital into illiquid assets, the lack of liquidity in large parts of the public markets and the decline of active institutional stock pickers has made many public equities almost un-investible to the remaining funds. At one point, I was quite hopeful that the bifurcation of markets into passive and private equity would have led to great opportunities for bottoms-up long term stock picking, but the momentum in performance required to maintain assets in a fund doesn't lend itself to holding an equity regardless of the valuation if it's remotely controversial or out of fashion. After just 8 months, the stock-picker and former Fidelity Magellan star fund manager Jeff Vinik closed his new fund this week as according to MSNBC, “investors told him that style doesn't work anymore”.

The illiquidity problem has become far more acute in Europe than the US. A recent study by Morgan Stanley has found that when defining liquidity as any equity that trades more than $100mio a day, European equities have fallen from 32% of global equity liquidity in 2006 to just 11% in 2018. Not only does the US and Asia have the equities of larger global champions such as Apple or Google, but the lack of IPOs and illiquidity only begets more illiquidity in Europe. European regulators should take note that a pillar of capital markets in Europe is in danger of being globally marginalised.

Many firms are not asking themselves why risk going public with the associated costs, regulatory hurdles and transparency requirements when there are large pools of private market capital available? Or the flipside, why do we keep the firm listed when the valuation doesn't reflect the value of the business?

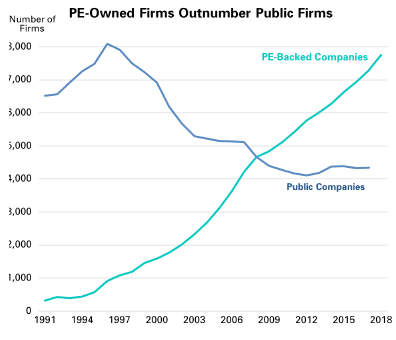

As a reflection of this, in less than 20 years the average age of listed companies in the US has risen significantly and the total number of publicly listed firms is down by 50% all the while the number of private firms held by private equity firms has rocketed.

Without the short-term investment horizon of public markets to worry about and access to low cost capital, many firms are staying private longer, concentrating the wealth creation of equities in growing alternative investment funds that can charge large fees before the equities become publicly investible.

Stylistically, the equity market landscape now has an under belly of undervalued and underrepresented firms, but the WeWork debacle is an exception to the stay-private-for- longer trend and unlikely to decrease the discounts to intrinsic value for mid and small cap publicly listed equities for the foreseeable future.

Notes

- IPO age and market capitalisation data: company filings and historical share-price records at the time of each listing.

- Alternative assets under management by asset class: Preqin.

- US public versus PE-backed firm counts: World Federation of Exchanges, Federal Reserve, SEC, Thomson Reuters Eikon, Milken Institute, March 2018.

- European equity liquidity share: Morgan Stanley, 2019.